UKKO Kevytyrittäjä

UKKO Kevytyrittäjä UKKO Yrittäjä

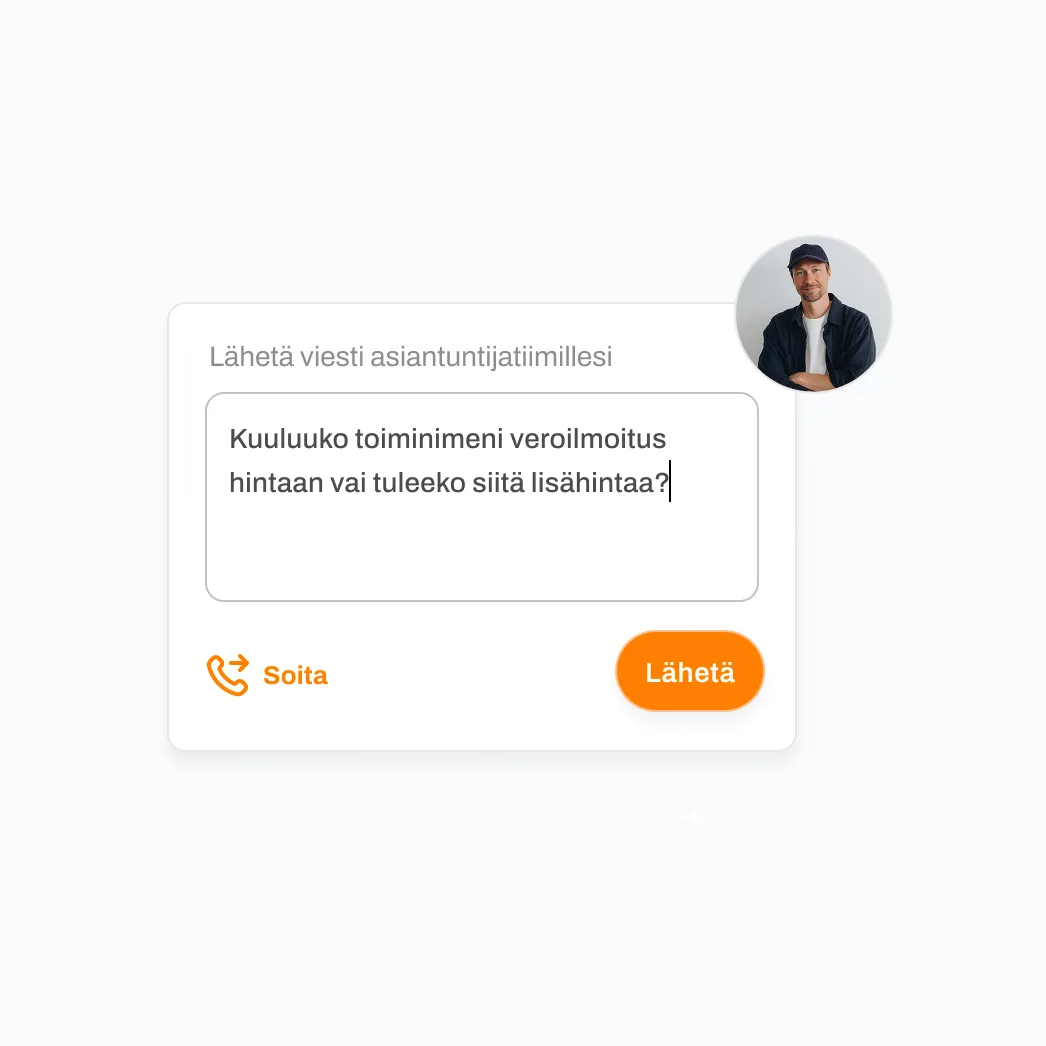

UKKO Yrittäjä Asiakaspalvelu

Asiakaspalvelu

UKKO Kevytyrittäjä

UKKO Kevytyrittäjä UKKO Yrittäjä

UKKO Yrittäjä

Toiminimen kirjanpito ja laskutus – helposti ja luotettavasti

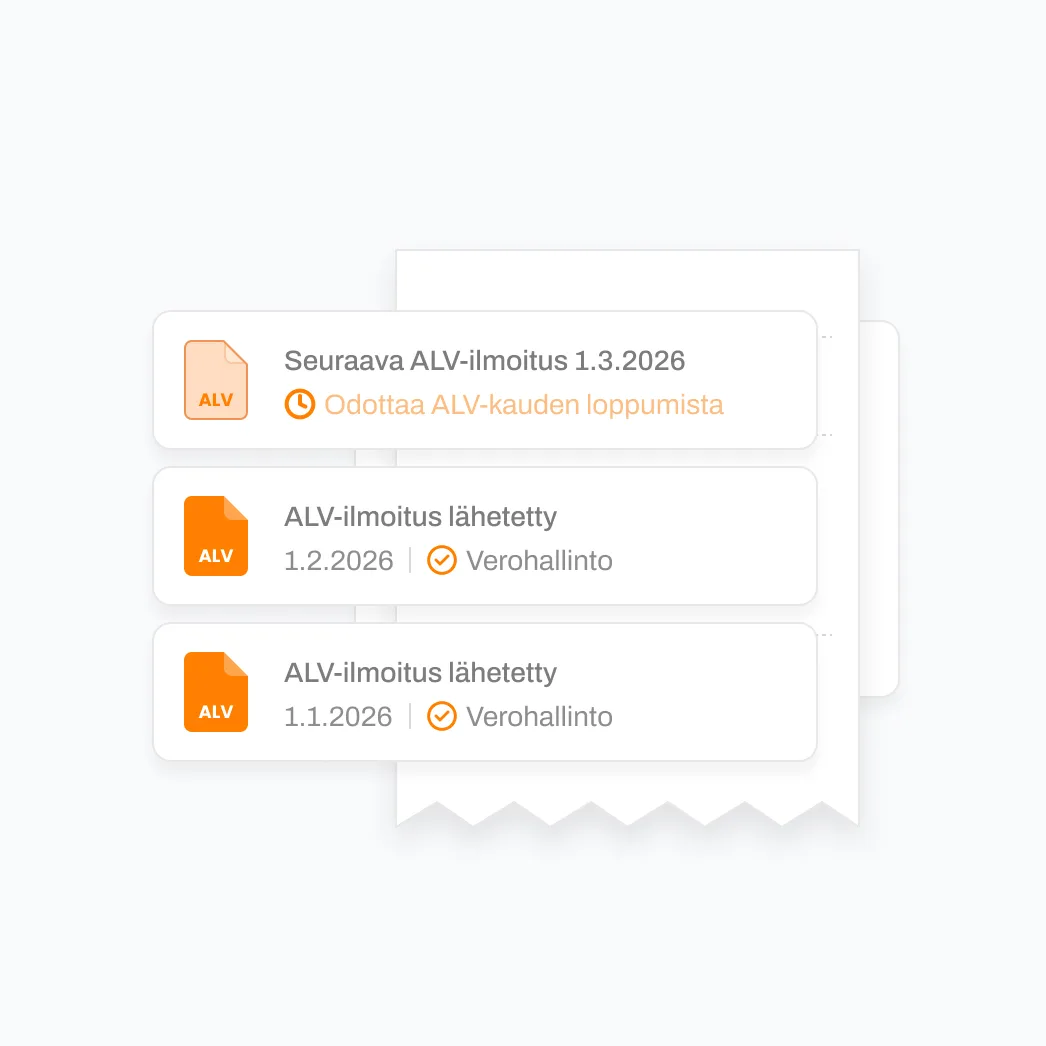

Luo laskut, seuraa tulojasi ja anna meidän hoitaa toiminimesi kirjanpito sekä viranomaisilmoitukset. Saat kaiken tarvittavan toiminimen taloushallintoon yhdestä paikasta – ilman turhaa säätöä.

- Kirjanpito ja laskutus

- ALV- ja veroilmoitukset

- Kesäetu: 12 kk – 20 %!